There are two schools of thought on what has been termed as the ‘funding winter’: one says that it is very much here and will remain for some months; another group believes it is hype touted by pessimists.

But the truth lies in data, in hard facts. And not just facts at a helicopter level but in granular details – because the truth almost always appears when one digs deep.

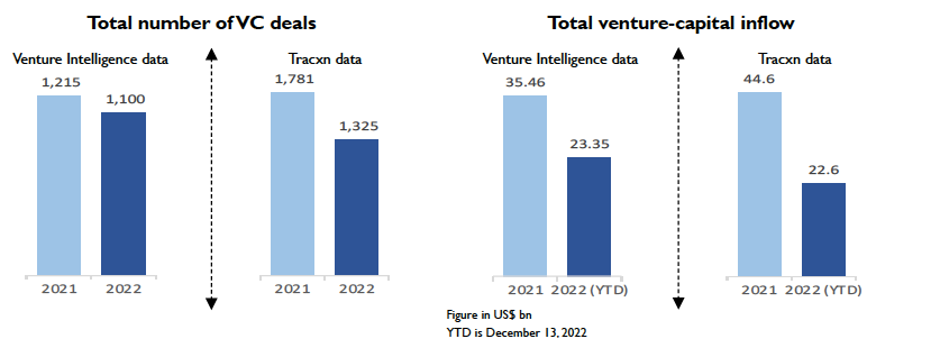

While fundraise has been less difficult for most VC firms, investments in startups have definitely slowed down. This downward trend is clearly reflected in data published by Venture Intelligence (VI) and reported in The Economic Times in December 2022.

On an annualised basis, investments are down by 10%-20%, depending on whether you look at data from VI or Tracxn. The corresponding numbers, when it comes to the quantum of capital deployed, ranges between 30%-50%.

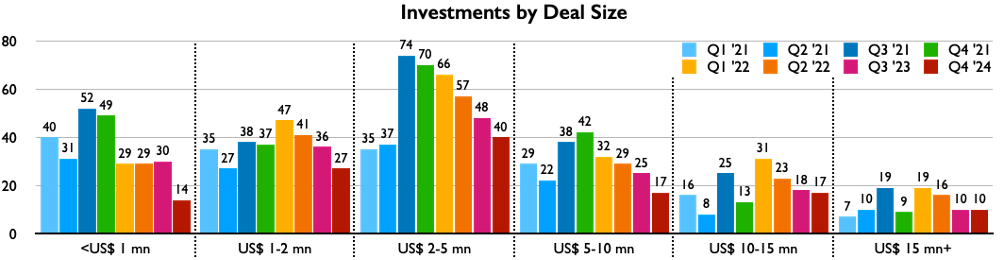

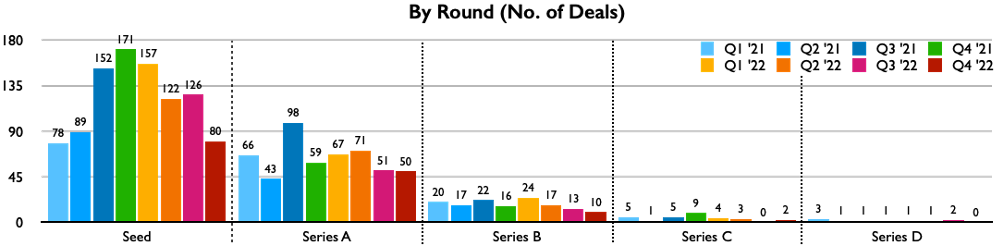

However, quarterly data reveals a steady downward trend that isn’t obvious if one limits the analysis to annualised statistics, as seen above.

Investments in early-stage startups are down from its peak of Q421/ Q122 by as much as 40-50% across the board, irrespective of round sizes and have been in a secular downtrend since peaking in early 2022.

This is also clearly visible in the graph below, which captures the velocity of investments. Here the contraction is upwards of 50% from the peak, across different stages of investments.

There is, however, a silver lining in these dark clouds: with VC firms sitting on what is called ‘dry powder’ or ammunition in the form of funds to invest, startups with realistic business models, genuinely deep technology (at least for us at YourNest) and committed founders with ethical practices are likely to get funded in the coming months.

Our best investments have happened when the world was shying away from writing cheques: a case in point being the YourNest SOAR program, the country’s first rapid-funding program which we launched in May 2020, during the Covid-induced lockdown. Some of the investments that we made as part of this program – such as Dozee, UptimeAi and Datamotive – have really scaled up well on the back of favourable digitisation trends in the post-Covid era.

At the fund level, we are sitting on more than 70% dry powder, to be deployed in the coming quarters, and the current funding slowdown is helping us access the best founders out there, that fit into our DeepTech, IP-led investment thesis.

Spring is coming… not just seasonally but in funding too. So, hang in there and take care. And remember that both God and the Devil are in the details.

Data source in quarterly graphs: Tracxn